Absolutely absolutely nothing.

Absolutely absolutely nothing.

That is the response to the title’s concern. It is also what hedge investment people receive in substitution for spending exorbitant costs.

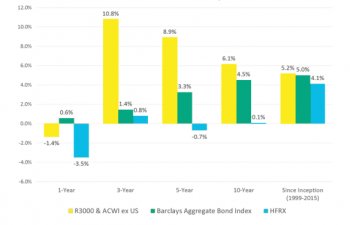

The chart the following talks about historical performance of hedge funds (blue bars) in accordance with diversified shares (yellow bars) and bonds (green pubs). It’s obvious that hedge investment overall performance happens to be relatively bad.

Asset Class Performance Comparison

Biases in Hedge Fund Information

The remarkable underperformance of hedge funds is pretty amazing thinking about the survivorship and backfill biases when you look at the index information that skew hedge investment returns up by 3% to 5percent annually.

Survivorship prejudice refers to hedge investment indices only showing comes back won by funds presently into the list. The list doesn't add funds that formerly reported returns but ended reporting because poor performance. The implication is that hedge resources just report if they are successful preventing reporting after they have actually a string of bad results, causing the list returns being unnaturally large.

Backfill prejudice also has dramatic impact on various hedge investment indices, including the HFRX international Hedge Fund Index when you look at the chart above. Backfill prejudice occurs when an index provider adds a fresh fund for their list and “fills in” prior returns of this fund (that are presumably good). For hedge investment supervisors, this usually means setting up a fund with seed money and waiting to report outcomes until comes back are sufficiently large to begin advertising and marketing the investment, thereby raising cash with the attraction of powerful previous performance. The end result is a procedure that overstates comes back.

Both biases stem from proven fact that hedge resources aren't needed to report their overall performance — all reporting is completely voluntary. Whether you look at an aggregate list including the HFRX Index or during the performance of a specific method, hedge funds report information showing higher performance than had been in fact recognized.

Both biases stem from proven fact that hedge resources aren't needed to report their overall performance — all reporting is completely voluntary. Whether you look at an aggregate list including the HFRX Index or during the performance of a specific method, hedge funds report information showing higher performance than had been in fact recognized.

General Skill Trumps Absolute Skill

Don’t misunderstand me, you can find wise hedge resources supervisors online. However, absolute ability features less to do with the likelihood for success than relative ability in which everybody is competing tough for a shrinking pool of excess returns.

Many hedge investment people believe they can determine a supervisors in advance. Perhaps some of these statements problem.

“We only find the most readily useful supervisors.”

“Our process is second to none.”

“We gain access to managers and information that other individuals don’t.”

As well as being above average doesn't always convert to outsized comes back. The circulation of comes back isn't an ordinary, also distribution; as an alternative, returns are greatly skewed so that a handful of supervisors break the industry by a substantial margin.

The Yale Model

David Swensen, CIO at Yale University, developed a model (popularly known as the Endowment Model or Yale Model) based on modern portfolio theory that invests heavily in alternative and illiquid investments. Swensen’s success at Yale has furnished the hedge investment business with a typical example of the reason why people is making use of Swensen’s products and strategies. Sadly, replicating the Yale Model is unrealistic for the vast majority of individual and institutional people.

Yale (and a handful of choose rivals) features a complete group dedicating 100per cent of their time to hedge fund analysis. Many household workplaces or monetary consultative businesses only have 1 or 2 visitors to devote to choices, and the ones men and women usually have other duties, also. The job threat for the majority of monetary advisers can be significantly more than when it comes to Yale endowment employees, leading to an increased probability of overall performance chasing and herding behavior.

The Yales worldwide have actually unprecedented accessibility managers and a level of transparency beyond published revisions that other people merely don’t get. Including, these big people get day-to-day holdings reports or perhaps the first call from a manager when something is wrong.

YOU MIGHT ALSO LIKE

Share this Post

latest post

-

-

Navigating the Landscape of Hedge Fund Strategies October 3, 2025

Navigating the Landscape of Hedge Fund Strategies October 3, 2025 -

Hedge fund CFO Compensation August 20, 2017

Hedge fund CFO Compensation August 20, 2017 -

Hedge fund Melbourne June 5, 2017

Hedge fund Melbourne June 5, 2017 -

Steel Partners hedge fund June 9, 2018

Steel Partners hedge fund June 9, 2018 -

Hedge fund performance fees April 1, 2019

Hedge fund performance fees April 1, 2019 -

Top hedge funds New York April 26, 2016

Top hedge funds New York April 26, 2016 -

Types of hedge fund strategies September 1, 2016

Types of hedge fund strategies September 1, 2016 -

Portfolio manager hedge funds January 16, 2017

Portfolio manager hedge funds January 16, 2017