Some time back, threat parity ended up being all the rage among institutional investors. And today, by way of a raft of shared resources floated over the past five years, retail people are able to tap into the strategy.

What’s threat parity? Quite simply, it's a profile allocation technique designed to restrict risk by overweighting lower-volatility possessions. You can see the appeal of this method to endowments and foundations. These institutions have to conserve capital in perpetuity. Volatility, particularly the kind seen in the aftermath regarding the Great depression, is crippling.

But just one form of volatility is truly bad—the downside kind. Upside volatility, you’d believe, ought to be welcomed. And therein lies the situation with risk parity: a valuable asset which falling low in cost, so long as it displays low volatility, will probably be considered less dangerous than an even more volatile financial investment persistently trending up. Basically, the model—with its unique consider risk—ignores comes back. At least within the near term.

For the majority of risk-parity models, allocation choices are derived from comparisons of portfolio assets’ standard deviations. Since stocks usually are more volatile than bonds, allotments to equities in a risk-parity profile are usually smaller than fixed income—the exact reverse of the classic 60-40 asset blend (a portfolio composed of 60 % stocks and 40 percent bonds). Within the last 5 years, that method seems high priced.

Here’s why: The “parity” into the model indicates the allocation regarding the low-volatility asset is raised to equal the effective risk of the high-volatility asset. Suppose, like, you want to build a simple two-asset profile comprising the SPDR S&P 500 ETF (NYSE Arca: SPY) therefore the iShares Core United States Aggregate Bond ETF (NYSE Arca: AGG) representing broad marketplace contact with domestic equity and fixed-income securities. If recent record shows SPY’s standard deviation at 18 per cent and AGG’s at 4 percent (much whilst was 5 years ago), we’d make our initial equity allocation hence:

s = σa/(σs σa

where, Ws = fat of SPY allocation;

σa = standard deviation of AGG;

and σs = standard deviation of SPY.

AGG’s body weight can then be determined simply by subtracting Ws from 100 %. By this technique, a risk-balanced portfolio could have been built five years ago with an 18 % allocation to SPY and an 82 per cent dedication to AGG.

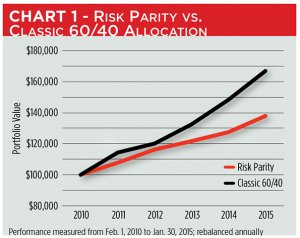

Therefore where’s the fee within? It becomes apparent if you contrast the portfolio’s worth over the ensuing five years to a vintage 60-40 portfolio. When rebalanced annually (the classic profile to its 60-40 norm plus the risk-parity portfolio to an allocation according to each preceding year’s standard deviations), the risk-parity portfolio’s collective gain falls far in short supply of the profit created by classic reallocation. Chart 1 illustrates just how a $100, 000 financial investment may have grown making use of each rebalancing approach. Over five years, threat parity produced a 38 per cent gain while a 60-40 allocation created a 67 % profit.

Share this Post

latest post

-

-

Navigating the Landscape of Hedge Fund Strategies October 3, 2025

Navigating the Landscape of Hedge Fund Strategies October 3, 2025 -

Hedge fund CFO Compensation August 20, 2017

Hedge fund CFO Compensation August 20, 2017 -

Hedge fund Melbourne June 5, 2017

Hedge fund Melbourne June 5, 2017 -

Steel Partners hedge fund June 9, 2018

Steel Partners hedge fund June 9, 2018 -

Hedge fund performance fees April 1, 2019

Hedge fund performance fees April 1, 2019 -

Top hedge funds New York April 26, 2016

Top hedge funds New York April 26, 2016 -

Types of hedge fund strategies September 1, 2016

Types of hedge fund strategies September 1, 2016 -

Portfolio manager hedge funds January 16, 2017

Portfolio manager hedge funds January 16, 2017