HEDGE-FUND bosses hardly ever double as cult authors. But an out-of-print guide by Seth Klarman, the employer of Baupost Group, offers for just as much as $2, 499 on Amazon. A scanned type of “Margin of Safety: Risk-Averse Value Investing Strategies for the Thoughtful Investor” happens to be circulating around exchanging flooring. One hedgie likens Mr Klarman's book on movie “Casablanca”: it's become a vintage.

HEDGE-FUND bosses hardly ever double as cult authors. But an out-of-print guide by Seth Klarman, the employer of Baupost Group, offers for just as much as $2, 499 on Amazon. A scanned type of “Margin of Safety: Risk-Averse Value Investing Strategies for the Thoughtful Investor” happens to be circulating around exchanging flooring. One hedgie likens Mr Klarman's book on movie “Casablanca”: it's become a vintage.

Exactly why are Wall Street dealers such avid visitors of Mr Klarman? Baupost, which manages $25 billion, could be the ninth-largest hedge investment worldwide. Since 2007 its assets do have more than tripled, as various other resources have wobbled. Baupost has received just two negative years (in 1998 and 2008) since it launched in 1982, and it is among the five most successful funds regarding life time returns (see chart), a really striking record provided its risk aversion. Longer shut to brand new people, Baupost counts elite endowments like those of Yale, Harvard and Stanford among its customers.

Soft-spoken and located in Boston, a safe distance from Wall Street mêlée, Mr Klarman keeps the lowest profile and hardly ever talks at industry shindigs. He's one of the most successful long-lasting performer into the hedge-fund industry that has was able to remain from the limelight.

Mr Klarman is a devotee of “value investing”, a discipline forged by Benjamin Graham (see article) and popularised by Warren Buffett, that involves buying stocks at a discount for their intrinsic value. He will look beyond equities for bargains—a good instance is Lehman Brothers, which after a year ago was Baupost's biggest distressed-debt position. In every investment he insists on a “margin of safety”, the buffer between what people pay for the stock and what they believe it is worth, so that they are shielded against unexpected events or miscalculations.

Mr Klarman initially became an acolyte of value investing as he worked at Mutual Shares, a value-investing mutual investment, as an intern and once again after he finished Harvard Business School. One of is own previous Harvard teachers then recruited him to run a family group company for him and three various other households, with a good investment pot of m (Baupost is short for for these households' surnames). Even though investment is notably bigger these days, Mr Klarman however works Baupost like a family group office. He is exceedingly risk averse; their main aim isn't stellar comes back but preservation of capital.

Mr Klarman initially became an acolyte of value investing as he worked at Mutual Shares, a value-investing mutual investment, as an intern and once again after he finished Harvard Business School. One of is own previous Harvard teachers then recruited him to run a family group company for him and three various other households, with a good investment pot of m (Baupost is short for for these households' surnames). Even though investment is notably bigger these days, Mr Klarman however works Baupost like a family group office. He is exceedingly risk averse; their main aim isn't stellar comes back but preservation of capital.

Various other ways, too, Baupost is certainly not an average hedge investment. It makes use of no leverage, which can be partly the reason why Mr Klarman isn't well-known for one stunningly lucrative trade, like George Soros's wager against sterling or John Paulson's contrary to the housing bubble. Baupost has actually few short jobs and sometimes keeps its opportunities for a long time, in place of days or months. Mr Klarman is diligent and confident adequate to do-nothing. He presently features around 30%—and was recognized to have as much as 50percent—of their profile in money. In 2008 Baupost was mostly of the companies that had the scale as well as the readily available money purchase up many assets from distressed vendors. “The ability to be one-stop buying an urgent vendor is extremely advantageous, ” he states.

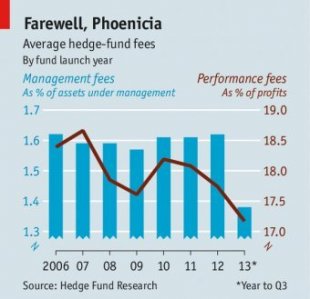

Offered Baupost's allure, it could quickly make a killing on charges. But Mr Klarman eschews the good “2 and 20” compensation framework typical of all hedge resources, which simply take 2percent of money as a management cost and 20% of gains. Alternatively, old investors spend “1 and 20”, and more recent ones (he's allow them to in two times, during the early 2000s and 2008) no more than “1.5percent and 20”.

YOU MIGHT ALSO LIKE

Share this Post

latest post

-

-

Navigating the Landscape of Hedge Fund Strategies October 3, 2025

Navigating the Landscape of Hedge Fund Strategies October 3, 2025 -

Hedge fund CFO Compensation August 20, 2017

Hedge fund CFO Compensation August 20, 2017 -

Hedge fund Melbourne June 5, 2017

Hedge fund Melbourne June 5, 2017 -

Steel Partners hedge fund June 9, 2018

Steel Partners hedge fund June 9, 2018 -

Hedge fund performance fees April 1, 2019

Hedge fund performance fees April 1, 2019 -

Top hedge funds New York April 26, 2016

Top hedge funds New York April 26, 2016 -

Types of hedge fund strategies September 1, 2016

Types of hedge fund strategies September 1, 2016 -

Portfolio manager hedge funds January 16, 2017

Portfolio manager hedge funds January 16, 2017