Just how Do I Need To Tactically Allocate my Assets?

A lot of people ask this question because their wide range grows additionally the few lending options expands exponentially. To be able to produce an answer, people pay cash to expert finance geeks which usually present complex treatments as an answer to the asset allocation issue. Last year, when I ended up being expected to provide a seminar on the subject during the, we created a tongue-in-cheek name for this: “Beware of Geeks Bearing Formulas.”

Within quick research piece we explore this seminar thoroughly. Our goal as evidence-based investors, and not story-based people, is always to set the record straight on worth of complexity in the framework of asset allocation.

Bottom line: simple appears to be better.

Defining Tactical Investment Allocation (TAA)

Precisely what is tactical asset allocation? I like to work backward to ahead, because it helps develop the idea.

Allocation (A): Our baseline, or fixed allocation to possessions in our universe. E.g., 50per cent stocks, 50percent bonds, rebalanced yearly. Asset (A): monetary assets that can be traded with reasonable liquidity. An extremely important component of being “tactical” will be fluid, which signifies that hedge funds, exclusive equity, and other asset classes with limited exchangeability legal rights is avoided inside context of “tactical” asset allocation. E.g. Shares, bonds, products, options (if fluid). Tactical (T): altering our baseline allocation predicated on some tactical rules. E.g., 50percent shares, 50percent bonds –> 30per cent stocks, 70% bonds predicated on an industry valuation sign.So there you have it, tactical asset allocation is tactically buying fluid assets being beat a static standard allocation.

Fundamental Investment Classes:

There's an old trader adage that you ought ton’t put your entire eggs in one container. For my classes, we diving into correlation mathematics to prove this time (see below), however the conceptual benefit of diversification is grounded in common good sense.

But how do we identify the eggs that go into our variation basket?

Meb Faber features in the Ivy Portfolio book, and reemphasizes in the brand-new guide, that you don’t have to get elegant when it comes to asset class selection. One can capture the big muscle movements around the globe by simply allocating across 5 asset courses:

One can capture the big muscle movements around the globe by simply allocating across 5 asset courses:

We label the return series as follows through the analysis:

SP500 = SP500 Total Return Index EAFE = MSCI EAFE Complete Return Index REIT = FTSE NAREIT All Equity REITS Total Return Index GSCI = GSCI Index LTR = Merrill Lynch 7-10 12 months national Bond Index Common Asset Allocation Techniques

Common Asset Allocation Techniques

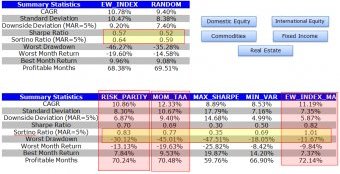

We discuss five common asset allocation strategies that are generally utilized in one form and/or various other by academics and/or professionals.

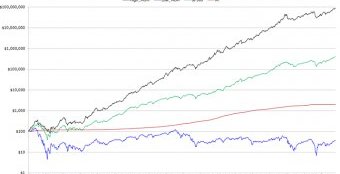

1. Tangency Portfolio/ Maximum Sharpe Portfolio

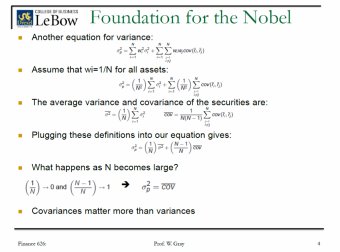

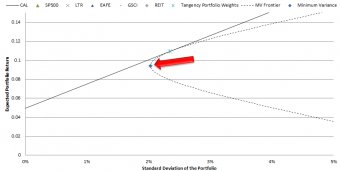

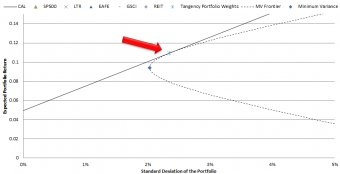

inspired by ‘s work on mean-variance-analysis during the early 1950’s, identified the suitable trade-off between threat and reward for a profile. Needless to say, the underlying presumptions providing given that foundation for this alleged “optimal” algorithm extend the imagination, nevertheless the intellectual construct and principles are dependable.

The punchline from modern-day profile concept could be the alleged “tangency profile.” This profile is identified because of the “x” with a vertical line through it and sits regarding the CAL (money allocation line). For anyone that haven’t taken an investment management program in a while, the CAL signifies all combinations of risk-free price additionally the tangency portfolio. These are “optimal” portfolios because there is no possible option to achieve a higher risk/reward. The perfect allocation loads for a 100% threat investor (i.e., no allocation to risk-free bonds) are the tangency profile weights.

The results are hypothetical results and NOT an indicator of future outcomes and don't express returns that any buyer in fact achieved. Indexes are unmanaged, don't mirror management or trading charges, and something are unable to invest straight in an index. More information regarding the building of those results can be acquired upon demand.

YOU MIGHT ALSO LIKE

Share this Post

latest post

-

Anonymous Chatting as a Modern Way to Socialize June 8, 2026

Anonymous Chatting as a Modern Way to Socialize June 8, 2026 -

-

Navigating the Landscape of Hedge Fund Strategies October 3, 2025

Navigating the Landscape of Hedge Fund Strategies October 3, 2025 -

Hedge fund CFO Compensation August 20, 2017

Hedge fund CFO Compensation August 20, 2017 -

Hedge fund Melbourne June 5, 2017

Hedge fund Melbourne June 5, 2017 -

Steel Partners hedge fund June 9, 2018

Steel Partners hedge fund June 9, 2018 -

Hedge fund performance fees April 1, 2019

Hedge fund performance fees April 1, 2019 -

Top hedge funds New York April 26, 2016

Top hedge funds New York April 26, 2016 -

Types of hedge fund strategies September 1, 2016

Types of hedge fund strategies September 1, 2016