By Andrew Beer

By Andrew Beer

New products are sold on a story. For alternative multi-manager mutual funds – the majority of that have launched since 2012 – the pitch goes something similar to this: we can get a hold of top level hedge fund managers to operate different alternative financial investment methods – equity long/short, general value, macro, etc. – within a ‘40 Act investment and provide “hedge fund overall performance with daily liquidity, reduced charges and much better transparency.”

Is this realistic? Most likely, the ‘40 Act framework puts numerous limitations on what those supervisors can invest – limits on shorting, illiquid possessions, types and control. Skeptics believe managers have to battle with one-hand tied up behind their particular backs. AMMF marketing and advertising teams countered that fee cost savings would offset any lost performance. Much more hostile players argued that retail investors would emerge ahead.

Really, the info is in and, as it happens, constraints matter. Lots. To simplify, from 2012 through 2015 AMMFs:

- Returned about 2per cent yearly internet of fees

- Underperformed hedge funds of resources after costs by 200 bps per year

- Fees and costs consumed more than half of comes back

- Comes back to investors had been generally speaking taxable at increased price

a discussion associated with methodology and outcomes uses.

A Brief History

The AMMF gold-rush banged off in 2012 when Fidelity launched that it would allocate $600 million to Arden resource control for a newly-formed AMMF. The knock on some current AMMFs ended up being they could just attract B and C people to control the sleeves (at 1% vs. the 2/20 quality hedge investment managers expect). But Arden, with Fidelity behind them, elevated the game. Now, every hedge investment must at least consider it. With defined advantage plans in inexorable decrease, and defined contribution programs rising, top tier supervisors could build a track record as a sub-advisor in anticipation of a flood of DC and retail assets – without doing it directly and possibly killing the 2/20 fantastic goose.

Many translated this since the start of a deluge from DC plan assets. 10% of trillions of dollars is … loads. Fidelity, a leader when you look at the target date fund room, would pave just how. Quickly various other huge DC people had to leap in. Within months of the Arden launch, lots of new AMMFs had been into the works.

But was this a market wide mind fake? The most obvious problem is costs: big DC plans balk at having to pay 250 bps for everything. Current division of work rulings won’t help. Mediocre overall performance eliminates any sense of urgency. As the doorways to DC program assets stay closed, many sponsors changed their particular advertising and marketing attempts towards retail/RIA networks. This is how we remain today.

Performance Leads To Increased Detail

We currently track the overall performance of 32 shared funds that fit the AMMF model: a manager hires sub-advisors to run hedge fund-like sleeves. One fund began around 2002, but the majority had been launched since 2012; just before after that, how many funds is adequately reduced we try not to think about the outcomes conclusive. For each twelve months, we take an equally weighted profile of funds having complete 12 months performance data and calculate the net of charge return. We compare those results to the HFRI Fund of Funds Index – a great representation of this performance of institutional hedge investment portfolios but possibly with a slightly higher fee structure.

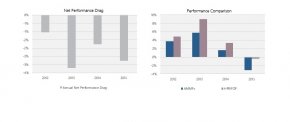

The debate “you’ll allow it to be back fee cost savings” simply will not be true. Once you lose 300 bps from the top (see chart below), 100 bps approximately in cost savings does not get you back to even.

Exactly what this shows is the fact that lack of limitations in hedge fund automobiles is an essential component of how they can make money with time.

Conclusion

Let’s summarize the results in a way. From 2012 through a year ago:

- Before costs, hedge resources returned only a little over 7.5percent per year – not so bad in a zero rate of interest environment.

- Those exact same, or similar, supervisors generated comes back of approximately 4.5% per year inside the constraints of AMMFs – quite simply, limitations cost 300 bps or virtually 40percent of returns.

- AMMF people paid costs and expenditures of 2.6percent typically, or higher than 1 / 2 of gross comes back.

- AMMF people wound up with yearly comes back of approximately 2percent per annum before fees.

- Almost all gains had been taxable, frequently at large prices.

To be reasonable, there are a few standout performers – Blackstone’s product leaps in your thoughts – as you will see in virtually any population of funds. Some growing aches – like interestingly high beta through the October 2014 drawdowns – were mainly remedied by last summertime. But various other risk management issues caused a few resources to get rid of 2015 down dual digits – tough to stomach as soon as the pitch is based on constant comes back and money preservation. With hot money in search of the exit, expect some sponsors to take the wounded this season.

And in addition, the keep from numerous possible investors was “why trouble?” The variation argument drops aside if many hedge investment alpha is lost into the repackaging. Indeed, it's been a really, extremely hard financial investment environment; however, high expectations are warranted whenever costs tend to be large, techniques opaque, and effective income tax rates punishing.

YOU MIGHT ALSO LIKE

Share this Post

latest post

-

-

Navigating the Landscape of Hedge Fund Strategies October 3, 2025

Navigating the Landscape of Hedge Fund Strategies October 3, 2025 -

Hedge fund CFO Compensation August 20, 2017

Hedge fund CFO Compensation August 20, 2017 -

Hedge fund Melbourne June 5, 2017

Hedge fund Melbourne June 5, 2017 -

Steel Partners hedge fund June 9, 2018

Steel Partners hedge fund June 9, 2018 -

Hedge fund performance fees April 1, 2019

Hedge fund performance fees April 1, 2019 -

Top hedge funds New York April 26, 2016

Top hedge funds New York April 26, 2016 -

Types of hedge fund strategies September 1, 2016

Types of hedge fund strategies September 1, 2016 -

Portfolio manager hedge funds January 16, 2017

Portfolio manager hedge funds January 16, 2017