Benjamin Tal never ever imagined himself the defender of this Canadian housing industry, nevertheless the deputy main economist at Canadian Imperial Bank of Commerce squared down Thursday against a U.S. commentator to call-out what he views as our bloated housing market.

Benjamin Tal never ever imagined himself the defender of this Canadian housing industry, nevertheless the deputy main economist at Canadian Imperial Bank of Commerce squared down Thursday against a U.S. commentator to call-out what he views as our bloated housing market.

The Thursday early morning discussion, sealed into the public, was part of a global investor conference, held in conjunction with the Global financial Fund springtime meetings in Washington.

Mr. Tal encountered Seth Daniels, handling partner of JKD Capital, just who feels Canada is set for an important housing correction followed by a recession — one thing operating the “short Canada” philosophy that developed inside U.S. and globally.

“Everything is general because I’m not exactly the essential bullish man [on housing], ” Mr. Tal, informed the Financial Post in a job interview each day prior to the meeting. “The just concern could be the magnitude.”

The real difference is important because people overseas shorting the Canadian marketplace are able to affect the economy by creating enough unfavorable sentiment to impact consumers, said Mr. Tal, who's needed a modification of 10per cent to 15percent in rates.

He offered his argument to a digital who’s who of leading U.S. hedge-fund managers many leading economists. One of the market had been Paul Leff, handling director of Perry Capital, and Myron Samuel Scholes, a Nobel Laureate in economic sciences famed for Black-Scholes model that offered a framework for valuing choices.

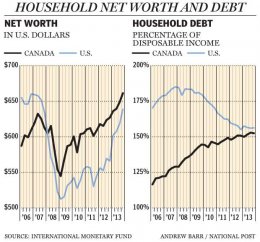

The theory the type of who would like to short Canada is the fact that a credit bubble is forming right here and that may lead to an economic failure which much bigger than the actual bubble. The experts point to debt amounts which can be however practically anyway time-highs with family debt about 164per cent of disposable income.

The theory the type of who would like to short Canada is the fact that a credit bubble is forming right here and that may lead to an economic failure which much bigger than the actual bubble. The experts point to debt amounts which can be however practically anyway time-highs with family debt about 164per cent of disposable income.

Into the interview, Mr. Tal stated part of the problem for folks shorting Canada is they don’t gain access to the exact same information he's about the market as the government isn't offering adequate openly accessible information.

“It’s not merely good enough to consider the credit you need to see just what sorts of credit our company is discussing, ” stated Mr. Tal, whom made headlines this thirty days with requires more data on the housing market and tasks.

As a CIBC economist, he can get a fairly great read on the credit of Canadians because his bank features a considerable amount associated with the marketplace nationwide.

While home prices consistently reach all-time highs month after month, Mr. Tal claims that itself isn't reasons to think a collapse is imminent.

He states the whole issue of overbuilding is dependant on simplistic reports of individuals seeing cranes everywhere and adds that new-home building was only 10percent above family formation in the last decade whilst in the U.S. it absolutely was 170% ahead of the market there collapsed.

In Mr. Daniels, he encountered a person who firmly thinks the Bank of Canada in addition to federal government are together accountable in part the collapse he anticipates. He feels within the Austrian business cycle concept that maintains business rounds depend on exorbitant development in credit because of government-driven reasonable credit prices. Mr. Daniels states he was capable make money from this during 2008 financial crisis.

“The part of government-sponsored credit insurance coverage in exacerbating the artificial credit boom is exclusive to Canada. I’m not aware of every other economic climate in the field that has been distorted to these types of a degree by credit insurance coverage. So a big an element of the Canadian credit bubble is tracked on presence of the [Canada] Mortgage and Housing Corp., ” he said in a current interview.

Consumers with less than a 20% down payment in Canada must get home loan default insurance — market for which CMHC maintains vast majority control. That insurance coverage is backed by the federal government with a possible responsibility of up to $1-trillion once personal people are included.

Mr. Tal things to defaults in Canada becoming really below 0.2per cent, suggesting that even yet in the U.S. defaults at their particular worst reached just 6% to 7per cent of mortgages.

Share this Post

latest post

-

-

Navigating the Landscape of Hedge Fund Strategies October 3, 2025

Navigating the Landscape of Hedge Fund Strategies October 3, 2025 -

Hedge fund CFO Compensation August 20, 2017

Hedge fund CFO Compensation August 20, 2017 -

Hedge fund Melbourne June 5, 2017

Hedge fund Melbourne June 5, 2017 -

Steel Partners hedge fund June 9, 2018

Steel Partners hedge fund June 9, 2018 -

Hedge fund performance fees April 1, 2019

Hedge fund performance fees April 1, 2019 -

Top hedge funds New York April 26, 2016

Top hedge funds New York April 26, 2016 -

Types of hedge fund strategies September 1, 2016

Types of hedge fund strategies September 1, 2016 -

Portfolio manager hedge funds January 16, 2017

Portfolio manager hedge funds January 16, 2017