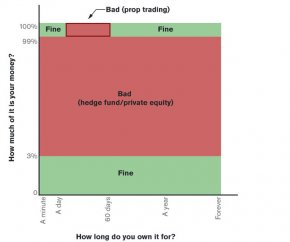

That chart is nonsense, that is partly my fault - do not go trade onto it or anything - but mostly the fault of the Volcker Rule. Fundamentally, if you are a lender, you can purchase assets utilizing your very own money - "proprietary" trading or investing - if you either plan to hold them for more than 60 days, or want to eradicate all of them rapidly to meet "reasonably anticipated near term needs of customers, customers or counterparties." However cannot buy possessions using a fund that contains a number of your hard earned money plus some of your clients' money - that is a "hedge fund" or a "private equity fund." Unless a maximum of 3 percent associated with profit the fund is yours. Then chances are you're good.

That chart is nonsense, that is partly my fault - do not go trade onto it or anything - but mostly the fault of the Volcker Rule. Fundamentally, if you are a lender, you can purchase assets utilizing your very own money - "proprietary" trading or investing - if you either plan to hold them for more than 60 days, or want to eradicate all of them rapidly to meet "reasonably anticipated near term needs of customers, customers or counterparties." However cannot buy possessions using a fund that contains a number of your hard earned money plus some of your clients' money - that is a "hedge fund" or a "private equity fund." Unless a maximum of 3 percent associated with profit the fund is yours. Then chances are you're good.

The chart is weird and stripey but try not to whine to me about any of it, i simply made the chart, maybe not the rule.

I've talked about Goldman Sachs's Volckerishness before, because it delights me. Plus it will continue to delight. Listed here is a tale about how "Goldman happens to be quietly discovering a number of new methods to place a unique money to the office in platforms that seem to stick to the proper side of Volcker, " that is quite simple to understand if you simply keep that chart in front of you. Goldman is investing its very own money, not customers' funds, therefore it is near the top of the chart. And it is purchasing things like "apartments in Spain, a mall in Utah and a European ink company, all of these the financial institution hopes eventually to market for a profit, " yet not (one assumes) within 60 days, so it is toward the best of the chart. Top right is green. Good to go.

This is the whole evaluation, but demonstrably you can easily complicate it more if you need. After all, that chart is ludicrous, which annoys the folks whom ... really ... whom made the chart:

Goldman’s merchant banking business is upsetting some regulators, just who be concerned that these types of opportunities do not proceed with the character associated with legislation, which is designed to reduce concentrated risks at banks, relating to individuals at three regulatory companies, who were perhaps not authorized to speak openly.

GUYS YOU WROTE THE RULE. There is no "spirit"! If the Volcker Rule "aims to reduce concentrated risks at banks, " then those green bits of the chart are a map of where it misses its aim. It seems odd to get upset at Goldman for that.

You can find arguments for turning the most effective right regarding the chart purple, and arguments for making it green. Ideal debate for modification might be simply the patchy appearance of the chart: the reason why would it not seem sensible to allow banks hold 100 percent of a thing, yet not 99 percent? If exclusive equity is just too dangerous for banking institutions, why would increasing their particular experience of it make sure they are less risky? That isn't necessarily a disagreement for forbidding business banking. It can be an argument against prohibiting bank-run private equity resources. Anything about that boundary doesn't look right though.

The actual happiness into the tale, though, comes whenever Goldman will leave the chart at the rear of. Notice just what occurred here:

Inside last half of 2014, Goldman invested about $800 million with two lovers for 144 resort hotels in Britain, and $200 million with two different lovers in the Southern Towne Center shopping mall in Sandy, Utah, among other huge opportunities.

That's not only Goldman spending its profit resort hotels and malls. Which is Goldman investing a mixture of unique money and its "partners'" money in accommodations and malls. That ... I mean, if you just dumbly consider my chart, that looks like the big red middle area. Goldman does not have 100 percent of the malls or resorts, though I bet it owns significantly more than 3 %.

But it is fine. Goldman doesn't have your can purchase 100 % of organizations it invests in. It may partner with other folks to get those companies. It simply can not spend anyone else's cash. It can't signal customers up for a fund, and then decide how to invest the fund. But it can determine how to invest a unique cash, then sign clients up to invest alongside it.

That's types of a tricky difference, is not it? You can't rather re-create a private equity fund that way, but you can get near. You invest some funds, your customers invest some money, you share the potential risks and the upside, you will get paid for putting the deal collectively. (Presumably Goldman's "partners" in those deals are not having to pay private-equity-like fees, but there's no guideline against Goldman getting better economics for sourcing or structuring discounts.) You must put an innovative new joint venture collectively for each and every deal, in the place of having one huge fund with one collection of lovers, and you're limited into the wide range of partners it is possible to bring into any package. In certain techniques this can be good - you get to select suitable lovers for every single deal, as opposed to investing everyone's cash indiscriminately - though it lacks the lasting committed capital, and continual charges, of a real personal equity fund. However, if you do it sufficient, it can kind of start to seem like a personal equity business.

The Volcker Rule recognizes this: One primary factor in identifying a permitted "jv" from a prohibited "private equity fund" is whether or not the fact holds it self down to be a personal equity fund. Which makes sense. You can't draw the distinction between what's permitted because of the Volcker Rule, and what'sn't, on compound. The substance for the guideline is in that chart, which seriously isn't really substantial. Technicalities are really all you have to continue.

This column will not always mirror the viewpoint of Bloomberg View's editorial board or Bloomberg LP, its proprietors and people.

YOU MIGHT ALSO LIKE

Share this Post

latest post

-

-

Navigating the Landscape of Hedge Fund Strategies October 3, 2025

Navigating the Landscape of Hedge Fund Strategies October 3, 2025 -

Hedge fund CFO Compensation August 20, 2017

Hedge fund CFO Compensation August 20, 2017 -

Hedge fund Melbourne June 5, 2017

Hedge fund Melbourne June 5, 2017 -

Steel Partners hedge fund June 9, 2018

Steel Partners hedge fund June 9, 2018 -

Hedge fund performance fees April 1, 2019

Hedge fund performance fees April 1, 2019 -

Top hedge funds New York April 26, 2016

Top hedge funds New York April 26, 2016 -

Types of hedge fund strategies September 1, 2016

Types of hedge fund strategies September 1, 2016 -

Portfolio manager hedge funds January 16, 2017

Portfolio manager hedge funds January 16, 2017