Given that both hedge investment supervisors and investors have accepted the concept of supplying absolute return products in a UCITS format, the question facing market individuals is whether or not the introduction of AIFMD will have exactly the same good impact on a. The solution to this question may help supervisors determine their strategic way of increasing assets in European countries.

Given that both hedge investment supervisors and investors have accepted the concept of supplying absolute return products in a UCITS format, the question facing market individuals is whether or not the introduction of AIFMD will have exactly the same good impact on a. The solution to this question may help supervisors determine their strategic way of increasing assets in European countries.

So as to make this determination, supervisors should:

Meanings

UCITS resources: resources domiciled in European countries and was able in line with the terms of the UCITS Directive

AIFMD resources: Funds domiciled in Europe and at the mercy of the terms of the AIFMD

Offshore resources: resources domiciled in a non-European offshore jurisdiction, generally Cayman isles, BVI, Bermuda, Jersey or Guernsey

Summary and considerations for supervisors

Summary and considerations for supervisors

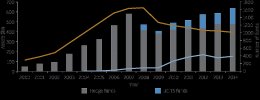

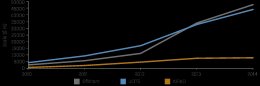

The landscape for hedge funds that are increasing capital in European countries has changed significantly since the financial meltdown. A once one-dimensional industry now has actually a wider number of regulating structures and a wider buyer base. The AIFMD and UCITS Directives have actually a significant impact on the way supervisors seek to improve assets while the people which they target.

Resource development from European countries because the economic crisis has come predominantly through the adoption by supervisors of UCITS framework. Applying this set up regulating model, supervisors have already been capable broaden their particular clientele to incorporate a sizable share of investors accessed through private-wealth station.

The development of AIFMD has brought the potential for greater transparency and disclosure but doesn't seem to took hold with people however. These funds continue to be bought predominantly by an investor base already more comfortable with offshore hedge resources. But without the emergence of a trigger for either the development of AIFMD resources by supervisors, or a corresponding increase in need for resources of the kind, we anticipate the adoption of AIFMD because of the market become sluggish.

By contrast, resources set up as UCITS have enjoyed better momentum in terms of both adoption by managers and increasing assets. Inside our view, particular catalysts surfaced following the economic crisis, which encouraged hedge investment supervisors to determine UCITS funds. Simultaneously, this offer happy a hitherto unmet demand from investors. Moreover, UCITS was already a well founded and generally recognized brand in its very own right.

Given this backdrop, there is much to think about for managers seeking to Europe for distribution.

Given this backdrop, there is much to think about for managers seeking to Europe for distribution.

Structural needs

Essential variations separate offshore/AIFMD and UCITS funds in terms of the financial investment guidelines, meaning that not all the strategies can be easily replicated into a UCITS wrapper. Managers have different options based on whether it's possible to create a UCITS or AIFMD investment.

Circulation

The use of AIFMD and UCITS may start new markets for managers to market their particular funds. They should consider:

Operational resources

YOU MIGHT ALSO LIKE

Share this Post

latest post

-

-

Navigating the Landscape of Hedge Fund Strategies October 3, 2025

Navigating the Landscape of Hedge Fund Strategies October 3, 2025 -

Hedge fund CFO Compensation August 20, 2017

Hedge fund CFO Compensation August 20, 2017 -

Hedge fund Melbourne June 5, 2017

Hedge fund Melbourne June 5, 2017 -

Steel Partners hedge fund June 9, 2018

Steel Partners hedge fund June 9, 2018 -

Hedge fund performance fees April 1, 2019

Hedge fund performance fees April 1, 2019 -

Top hedge funds New York April 26, 2016

Top hedge funds New York April 26, 2016 -

Types of hedge fund strategies September 1, 2016

Types of hedge fund strategies September 1, 2016 -

Portfolio manager hedge funds January 16, 2017

Portfolio manager hedge funds January 16, 2017